21 Mar What Ongoing Banking Turmoil and Market Pullbacks Mean for Investors

These banking system concerns add to the numerous challenges investors have faced in recent years. Over the past 12 months, investors have managed through inflation, Fed rate hikes, Russia’s invasion of Ukraine, and a bear market. In 2021, many were concerned over the sustainability of the economic recovery and excessive stock market valuations. In 2020, the pandemic and nationwide shutdowns threatened the economic and financial system, in addition to the well-being of everyday individuals. Many of these events occurred seemingly out of left field, catching investors off guard.

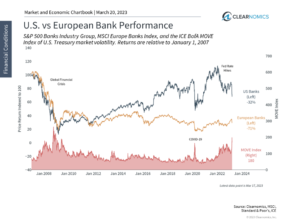

Banking system concerns have spread to Europe

Find this chart under “Financial Conditions”

Investors cannot invest in a market index directly, and the performance of an index does not represent any actual transactions. The performance of an index is not an actual client portfolio which is subject to the deduction of various fees and expenses which would lower returns. Past performance is not a guarantee of future results.

However, while there are unique circumstances behind the failures of Credit Suisse and Silicon Valley Bank, banking crises are not as unexpected as global pandemics and military invasions. Economics is often referred to as the dismal science because it only predicts crises after they occur. With the benefit of hindsight, these bank failures echo other collapses across history. Taking a broader perspective, the history of financial markets is full of episodes that have been well documented, including in the classic book Manias, Panics, and Crashes by Charles Kindleberger.

One theory is that the common thread across these episodes is the availability of money, the expansion of credit, and the eventual tightening of financial conditions. Like a sugar rush, the supply of credit and the flow of funds through the global financial system can drive asset bubbles, appreciating currencies, and risk-taking in a particular market or across a whole country. Sooner or later, however, there is a sugar crash as returns peter out, sentiment shifts, and conditions tighten. This not only occurred leading up to the 2008 housing crash and financial crisis, but over countless other episodes including the 1997-1998 Asian currency crisis when the hedge fund Long-Term Capital Management required a bailout, and the savings and loan crises from 1980 to 1994 when 1,600 U.S. banks failed.

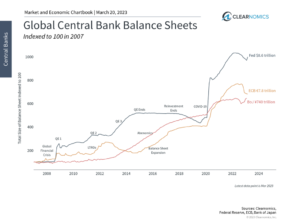

Central banks have tightened conditions over the past year

Find this chart under “Global Central Banks”

This suggests that while failed banks are not innocent bystanders – they often involve poor risk management and excessive risk-taking – they are also subject to macroeconomic trends just like any other corporation. When both the supply and demand for money by individuals and businesses are expanding, banks have strong incentives to extend more and more credit. As this compounds, it can lead to asset bubbles in real estate, the stock market, and more, which in turn further increase the appetite for credit. While this can continue for longer than expected, eventually it grinds to a halt.

Thus, it is no coincidence that this is occurring just as the Fed, the European Central Bank, the Bank of England, and other monetary authorities are removing liquidity from the system by shrinking their balance sheets and raising interest rates. Coupled with lower asset prices across the broad stock market, the tech sector, and areas like cryptocurrencies, it’s natural for financial stresses to build. The accompanying chart shows the reduction in central bank balance sheets across the globe over the past year. This has partially reversed in recent weeks as the Fed has provided hundreds of billions of dollars of additional support.

This does not mean that we will see a repeat of 2008 when the largest banks were significantly levered against what were believed to be safe securities. Today, these banks are much better capitalized and have broader deposit bases. For better or worse, regulators also have playbooks to be used at the first sign of trouble, as we have seen over the past few weeks.

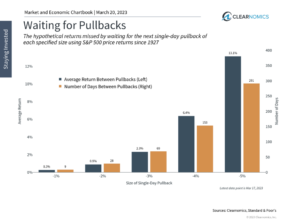

Waiting for market pullbacks often results in missed opportunities

Find this chart under “Volatility and Staying Invested”

For long-term investors, this reinforces the need to hold diversified portfolios with proper risk management. The S&P 500 continues to trade at the most attractive valuation levels in years and interest rates have been much more stable. Balanced portfolios have already performed better this year, preserving capital and benefiting from stronger bond performance.

The irony is that some investors are always waiting for an opportune time to invest in the market. However, when markets do temporarily fall, these same investors may be hesitant to take advantage due to the nature of each market crisis. Unfortunately, this is nearly always the case since markets usually pull back for a reason. What inevitably happens is that investors miss these opportunities when markets eventually recover, forcing them to wait for the next pullback.

History shows that it’s better to simply stay invested. The accompanying chart shows the effect of waiting for different sized one-day pullbacks. For instance, an investor that waits for a 3% pullback would have to wait 68 trading days on average, missing a 2.3% gain that would have been achieved if they simply invested and held on. These historical returns are even larger for bigger pullbacks, since markets tend to rise over time.

Additionally, investing does not need to be all-or-nothing – even beginning with a strategy like dollar-cost averaging can help investors take advantage of attractive valuations while spreading risk over time. So, while the past is no guarantee of the future, history is fairly clear on how investors should take advantage of market environments like the present.

The bottom line? The banking crisis is still evolving but is already quite different from 2008. Remaining patient and taking advantage of attractive opportunities is still the best way for investors to achieve their long-term financial goals.

Sorry, the comment form is closed at this time.