15 Jul Looking Out for Number One

April 5, 2019

By Sterling Neblett

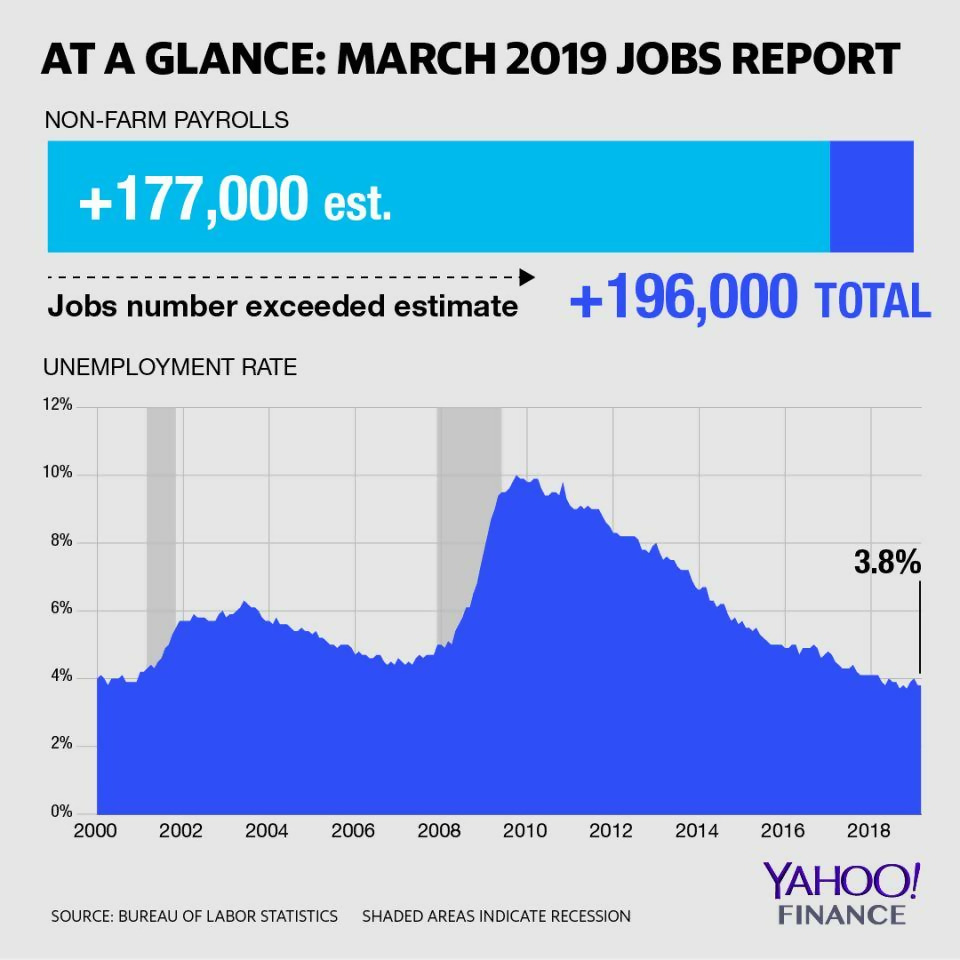

If the United States economy were an 18-wheeler, its driver might be singing along with Dave Dudley, “I got my diesel wound up and she’s a runnin’ like never before.” The driver would be looking at clear skies, and a wide-open highway, but an unreliable fuel gauge. Unemployment is at its lowest level this century, inflation remains at a historically low level; wage increases have only started to appear in this economic recovery, consumer confidence is near historical highs and this expansion has grown into one of the longest in United States history. For entrepreneurs, now may be a time to consider the plan that started the business, and how well that plan has worked in terms of current results versus initial projections. Business owners, concerned with day-to-day operations, may also benefit from taking a step back to appreciate the development of their creations.

Who Needs a Financial Plan?

A financial plan is a strategy to achieve the financial goals of an individual, a family or a business. Everyone needs a plan to achieve a stated financial goal, whether it is stored only in the planner’s brain, written on a napkin or professionally prepared, dated and signed. That plan may allow just enough to pay next months rent or enough to finance the education of the next generation. A financial plan is like a road map referred to regularly on the long, strange trip of life; the route is generally known, but decisions must be made while in route. The map displays many alternate highways and side roads but does not give updates on traffic or detours.

Wage and salary

workers need one financial plan; self-employed workers, business owners and entrepreneurs need two. Business owners must separate their personal plans from their business plans or the two will share the same fortune, positive or negative, long term and short.

Once the aspiring entrepreneur has stepped into the dream of financial independence, the tendency can be to fire up the engine and do whatever it takes to eat up the highway ahead without caring for the cargo. At an unexpected turn, the entire conveyance can be in danger of jackknifing. Personal financial stress can affect short-term business decisions which may have unintended long-term consequences, and which may not be best for the long-term success of either the business or the owner. For self-employed individuals, business owners and entrepreneurs who have an income stream established, a financial plan must include a number that indicates the current value of the business separate from the owner’s personal net worth.

What is a Business Worth?

A business valuation allows for better business decision making as to the best use of business funds and as a check on progress over periods of time from inception to present. The slope of the business’s valuation curve can also help to project the future value of the business. Common stock investment valuations can be automatically updated, their histories are readily available, and for most large, publicly traded companies, estimates abound as to their possible future values. Real estate is assessed for taxation, so records exist to chart growth in value, but when considering the sale of a business, an appraisal is required in order to set a monetary value.

Cost to Create

A business unique to the mind of its creator must be assigned a monetary value apart from the emotional ties and psychological attachments of the owner. To the one who thought it up, planned and started the business, its perceived value vary greatly from what the market will bear. But potential buyers exist who may simply wish to avoid the struggles of establishing the product, service or brand for a start-up. For the buyer, it may be a matter of opportunity cost—avoiding time lost in development.

Balance Sheet

All companies own assets, most have unavoidable expenses and many have debt to service. The net assets of a company, like the net worth of an individual, is the resolution of assets versus liabilities, debits versus credits. Most often the underlying value of a company is determined by its profits, but certain companies are formed with the expressed intent of holding appreciating assets. Storage companies are often used as “land banks” to hold property for possible further development or sale. Berkshire Hathaway (BRK-B) invests collected insurance premiums into attractively valued businesses rather than the more traditional practice of buying government-backed fixed-income securities.

Cash Flow

In order to most accurately value a business, it must be compared to other businesses on a common scale. Valuation based on cash flow considers how much money comes into a business, how much goes out, what is left and whether that number is growing or shrinking. The same methods fundamental analysts use to calculate the intrinsic value of a publicly traded common stock can be applied to evaluate a private business.

The Multiple of Cash Flow method involves the assignment of a multiplier to annual cash flow. Cash flow is defined as earnings before interest, taxes, depreciation and amortization (EBITDA). The multiplier is an estimate and takes into account growth of sales, profit margin, possibilities for expansion and projected capital requirements.

The Discounted Cash Flow method estimates future cash flow of a company and what a buyer might be willing to pay now for that future revenue. An appraisal of this type considers the time value of money and “discounts” those future cash flows to present value.

Transfer of Ownership

There are as many ways to transfer a business as there are types of businesses. Ownership of a sole-proprietorship might naturally be transferred to a member or members of the owner’s family, a partnership to partners, an S-corporation or a Limited Liability Corporation (LLC) to other shareholders, and a publicly traded company at the common stock market value. Partners and shareholders already have a clear picture of the value of the business, its potential and how important the seller is to the business.

Selling to a third party involves an evaluation of the business’s worth, but other delicate issues complicate the process. Plans to sell the business must be kept confidential because the knowledge that a business is for sale can affect the attitudes of employees, customers and competitors even though they may be potential buyers as well. One way to handle this situation is to hire a business broker who, like a real estate agent, is in business to assist both buyers and sellers.

Preserve and Protect

A financial plan for a business owner must also include allowances for the unforeseen. For most entrepreneurs, the business is dependent upon its creator for management, guidance and inspiration. The most valuable asset most businesses have is the presence of the owner, so that must be the first asset to insure. A business owner needs life insurance for family protection, but also to compensate for the loss of the business founder. A Business Owner Policy provides property, liability, crime and medical insurance in one contract. A business savings account provides protection in case the big rig hits a bump in the road. Savings are also War Chest held in case an opportunity for expansion appears.

All Plans

All financial plans are intended as a guide toward selected financial goals. These plans are similar in that they must be monitored in order to make allowances for the effects of unforeseen circumstances. But every financial plan is as unique as the individual or business for which it is produced.

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the opinions of Spire Wealth Management, LLC, Spire Securities LLC or its affiliates. Investing involves risk, including the loss of principal. Past performance may not be indicative of future results.

Spire Wealth Management is a Federally Registered Investment Advisory Firm. Securities offered through an affiliated company, Spire Securities, LLC a Registered Broker/Dealer and member FINRA/SIPC

Sorry, the comment form is closed at this time.