06 Jun InvestmentNews: Will new smart-beta strategies boost target-date funds’ performance?

As seen on www.investmentnews.com.

As seen on www.investmentnews.com.

By: John Waggoner

Target-date funds are the Energizer Bunny of the mutual fund world. As the industry struggles furiously for investors’ money, target-date funds slide blithely by, with billions of dollars in new money flowing in. Now they’re adding a little extra juice: smart-beta strategies.

Some fund companies — most notably BlackRock Inc. — have begun to offer TDFs with smart beta (also called strategic beta), with the goal of improving returns. BlackRock’s LifePath Smart Beta fund suite ranges from 2020 to 2060 in five-year increments, and includes a fund for those in retirement. The difference: The funds for younger investors with a longer time horizon emphasize return-seeking factors, such as momentum, while the funds for clients approaching retirement stress risk-reduction strategies, such as low volatility.

“You seek higher returns when you’re young, and seek to reduce risk when you’re older,” said Nick Nefouse, head of the defined contribution investment and product strategy team at BlackRock. The fund uses BlackRock smart-beta ETFs as its building blocks. (It also has a “dynamic” suite using active management.)

But BlackRock, which rolled out its smart-beta offering in November 2016, isn’t the only company mixing smart-beta strategies into its target-date funds. PowerShares by Invesco launched a suite of asset allocation ETFs in February based on a targeted exposure to equities and fixed income, using its low-volatility ETFs as well as other PowerShares fundamentally constructed ETFs.

The overall universe of smart-beta funds now totals 1,488 mutual funds and exchange-traded funds, up from 655 in 2012, according to Morningstar Inc.

But not everyone is convinced strategic-beta strategies will boost target-date performance, and The Vanguard Group Inc. is among them.

“We’re always debating and kicking and re-kicking the tires, trying to build for what’s enduring for this cycle and the next,” said John Croke, head of multi-asset product management in Vanguard’s portfolio review department.

“What holds us back with adding smart beta to a target-date fund is that over time there can be severe periods of underperformance that would cause investors to abandon the strategy. It’s hard to find a strategy that will move the dial. And we’re not comfortable introducing an additional degree of risk and uncertainty.”

ACTIVE FUNDS

Net inflows into target-date funds Source: Alight Solutio

It’s too early to tell whether smart beta will improve investor outcomes. But one thing is certain: No one has overlooked the steady growth in target-date assets, especially actively managed fund companies. Target-date funds often funnel assets to a company’s active funds at a time when investors and advisers are fleeing them.

“In many cases, target-date funds are the lifeline for actively managed funds,” said Jeff Holt, associate director of management research at Morningstar.

TDFs are designed to provide basic asset allocation to neophyte investors, primarily those in tax-deferred retirement plans, such as 401(k) and 403(b) plans. At least in theory, they are better than typical beginner fund choices, such as money market funds or simply dividing money equally among all the fund choices offered.

“If a client tells me they only look at their 401(k) plan every five years, target-date funds are a great solution to keep them balanced and in an appropriate asset allocation for their time horizon,” said Kristin Sullivan, owner of Sullivan Financial Planning.

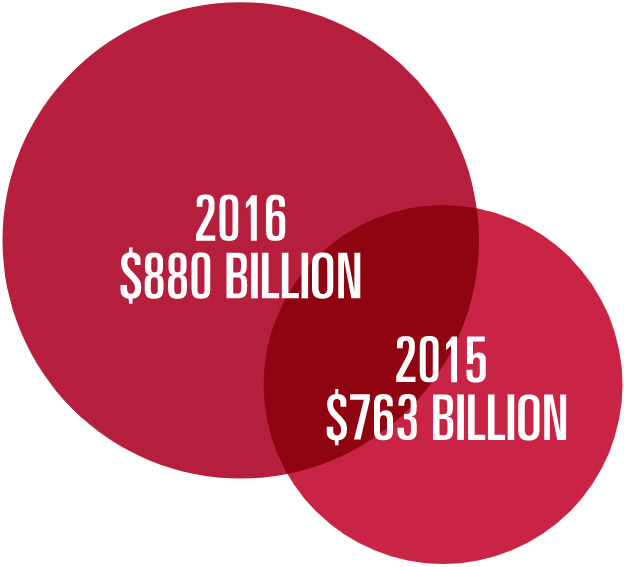

Target-date funds saw net inflows of $880 billion in 2016, up from $763 billion in 2015, according to Morningstar.

Part of that popularity reflects a trend among retirement plan providers to make TDFs the default option. Nearly 90% of retirement plans have a target-date option, versus 33% in 2005, according to Alight Solutions. About 60% of retirement plans use target-date funds as the default option for new participants.

(More: Fidelity, American Century adopting new TDF fee tactic as cost pressures grow)

Net inflows into target-date funds Source: Alight Solutio

“Asset managers see the target-date pie increasing, and their goal is to get a piece of that pie,” Mr. Holt said.

One way to increase their share is to have more offerings on the table, including smart-beta strategies.

Retirement plans with a target-date option Source: Alight Solutions

“Ten years ago, a target-date fund manager had one series of funds,” Mr. Holt said. “Now there are 40 firms offering 58 target-date series, with quite a few offering more than one series.”

PASSIVE MANAGEMENT

Retirement plans with a target-date option Source: Alight Solutions

An easy way for fund companies to broaden their target-date lineup is to offer a suite of TDFs that use all passively managed components, with low costs and high reliability.

Fidelity offers the Fidelity Freedom target-date series as well as the Fidelity Freedom Index series. Others, such as Principal, offer a mix of active and passive TDFs. And Natixis Global Asset Management recently rolled out a suite of funds that follow environmental, social and governance precepts, the Natixis Sustainable Future Funds.

But target-date funds of any stripe have several drawbacks, which advisers are quick to point out. First, investors often don’t use them properly.

Nearly half of all TDF users also invest in another asset class, said Winfield Evens, director of investment strategy at Alight Solutions. Doing so undermines the purpose of a target-date fund, which is to be a one-shot fund for retirement.

“Only 9% knew that a target-date fund rebalances over time, and that you only need to invest in one fund,” he said.

Other evidence shows that investors tend to outgrow target-date funds. “New folks who are defaulted in don’t have a complex life; it’s an easy choice.” Mr. Evens said. “But a 45-year-old doesn’t have an easy financial plan.”

Not surprisingly, those who are fully invested in target-date funds have an average balance of $26,000, versus $137,000 for those who are not invested in target-date funds at all.

Another reason investors leave target-date funds may be the ongoing bull market. When the Standard and Poor’s 500 stock index has gained 15.4% a year for the past five years (including dividends), a 2020 target-date fund’s average gain of 10.8% may seem a touch disappointing, no matter how well it did on a risk-adjusted basis.

“People forget what a bear market feels like,” Mr. Nefouse said.

Because so many investors abandon target-date funds once they accumulate wealth, some advisers don’t recommend them.

“Typically, I don’t [recommend TDFs] because most people end up paying for something that they will never use,” said Eric Dostal, an adviser at Sontag Advisory. “By that I mean individuals typically are not invested in a target-date fund for long enough to take advantage of the glide path.”

1,488 number of smart-beta mutual funds and ETFs, up from 655 in 2012

But that’s not the only reason some advisers shy away from target-date funds. Part of it is professional pride: They figure they can create a better, more custom-fit portfolio for their clients than one tailored for a generic person whose retirement date falls within a five-year range, even those TDFs that involve smart-beta strategies.

“If I’m looking at it from an RIA’s point of view, are target-date funds what I’m going to use? Quite probably not,” Mr. Evens said. “I’d feel that I have tools and skills that are better.”

Sterling Neblett, founding partner at Centurion Wealth Management, put his concerns about TDFs this way: “Although target-date funds are an excellent choice for your typical nonprofessional investor, they do come with limitations and lack of customization,” he said. “Most target-date funds are comprised of one company’s funds, which may not have the top managers in each of the asset classes.”

LONG-TERM OUTLOOK

In addition, Mr. Neblett said, target-date funds limit your ability to overweight or underweight certain investment classes.

“Those types of decisions are left to the target-date fund, which typically takes a more long-term strategic allocation rather than shorter-term tactical allocations,” he said. “I still recommend clients use target-date funds in their own 401(k)s where we don’t have access to manage them.”

(More: Best- and worst-performing fixed-income funds)

Mr. Neblett does see room for smart beta in TDFs.

“I am an advocate of smart-beta strategies for certain asset classes, and do feel they would be beneficial in target-date funds,” he said.

Byrke Sestok, president and financial planner at Rightirement Wealth Partners, agrees.

“I personally do not use smart-beta target-date funds, but those strategies have merit,” he said. “What is important is that one selects an investment plan and rebalances with a purpose.”

Mr. Sestok usually recommends TDFs for clients who have a history of not rebalancing and reallocating assets in their accounts that he doesn’t directly manage.

“As a certified financial planner, my responsibility is to do everything possible to make sure my clients move closer toward their goals,” he said. “Target-date funds and balanced funds are a good way to make it easy for clients to complete their homework.”

Sorry, the comment form is closed at this time.