15 Jul Starting Over as a Newly Independent Woman

It happens; things don’t work out and actions must be taken to adjust and move on. A ship that has survived a violent storm at sea may have to undergo extreme adaptations before continuing its voyage. Passengers may be pressed into service; crewmembers promoted and a first officer may take the helm. But before determining an eventual destination and setting an appropriate course, those in charge of the ship must address its situation in terms of safety and seaworthiness, make necessary repairs and replenish the stores for the voyage ahead. Whether the storm that raised the havoc was death, divorce disability or dysfunction, most immediate needs must be dealt with first.

First Things First

It may have been expected but without a time certain, or it may be an unexpected shock. The first effects felt of a life-altering event like, death, divorce or disability may be physiological and psychological. Those needs must come first; as the flight attendants say, “put your oxygen mask on first, before helping others.” A doctor and therapist can help a newly independent woman sort the physiological and psychological effects needs from her priorities for survival. A financial planner can help her organize her financial situation and confront her immediate needs in terms of food, shelter and clothing.

Maslow’s Hierarchy Of Needs

Source: Wikimedia.org

Review

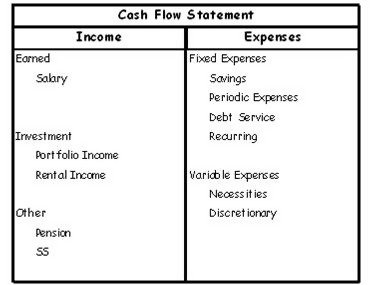

A professionally prepared Financial Statement will allow objective examination of immediate financial needs for survival and safety as well as for longer-term planning. Of most immediate importance is a Cash Flow Statement, which compares monthly income to monthly expenses and produces a number, positive or negative, surplus or deficit.

Source: rethinkingretirement.com

Repair

Once the gathering and sorting of financial information are done, projections can be made and adjustments suggested. The Cash Flow Statement produces a number by which the assets and liabilities on the Balance Sheet are adjusted, and indicates the monthly impact on Net Worth. The most immediate repairs can be made on the expense side of the cash flow statement. Those changes take effect as soon as the following month. For most women starting over, the income side of the Cash Flow Statement will take longer to establish and grow. Once expenses have been evaluated, and sources of income identified, longer-term planning can take place.

Replenish

A Balance Sheet compares the monetary value of assets owned to liabilities owed and produces a number for Net Worth. Survival of a long voyage may depend upon a ship’s ability to resupply. Ports of call must be plotted. A Balance Sheet, summed for Net Worth, can help to chart a course to future financial goals. The surplus or deficit produced by the Cash Flow Statement adjusts the Net Worth figured by the Balance Sheet and traces the course of financial progress.

Members of the financial crew may have been lost in the storm and need to be replaced. An estate attorney, upon the death of a spouse, will gather financial records in preparation for probate as will a divorce attorney leading up to a divorce settlement. Much of the work of gathering and sorting financial information, in cooperation with accountants, may already have been done. Those files, when provided to a Certified Financial Planner (CFP®) will allow production of a snapshot of the newly created financial, projections for the future as well as recommendations for modification.

Resume

Once a monthly budget has been established and future income has been secured, it will be time to choose financial goals and rank them by importance and timeframe. Savings must become a priority, but once savings have provided for short-term safety, investments can be planned to aid progress toward preset goals. Retirement savings are essential for the care of the elderly person the independent woman will become. Mothers will include funding of higher education; daughters will consider the needs of their parents.

Death

Nothing is more final than death and nothing like death can provoke so dramatic a change in the lives of those left behind. Some financial separation issues are resolved immediately upon a partner’s passing. Retirement accounts immediately become the property of the named beneficiaries. Life insurance payments are tax-free and are paid on a schedule determined by contract. Joint bank and investment accounts remain accessible, but single accounts in the deceased’s name may go through probate unless previous arrangements have been made. Probate can take nine months or longer to settle, which is another reason to secure immediate financial needs first.

Divorce

A newly divorced woman has often had time to prepare, at least from the date of service to date of the decree, but not until the final document is signed can precise financial planning begin. The divorce documentation provides a concrete source of information for the preparation of financial documents. But her most immediate concern may be how to put food on the table and get the monthly bills paid. That information is in the Cash Flow Statement.

Disability

The disability of a spouse or life partner can add the same challenges as death and divorce, but also includes the care of another person. A portion of the presence of the disabled person remains to be cared for, but the able partner must fill the portion that is absent. So the spouse of a newly disabled person picks up two new jobs in addition to the one she already had. If the disabling illness or injury has a prognosis, then an immediate financial plan should be created to cover the expected recovery period to compensate for additional expenses and loss of income.

Dysfunction

Sometimes things are just not working out, yet there is no end in sight. If a personal relationship with a life and financial partner has taken an undesirable turn, it may be time to think about where things could end up if the relationship ended. In a legal separation, some stipulations will be made about household and childcare expenses, so some information has been gathered that is necessary for a Cash Flow Statement. But asset ownership may be indeterminate until the divorce decree is dated. A lawyer, in preparation for a divorce, will want to put a value on the couple’s assets and so will look at the big picture. During such a period of uncertainty, a marriage counselor can work to preserve the union, but can also begin a conversation about terms of a final split.

Be Prepared

Personal financial planning for women is easier than planning a life because numbers are involved and numbers don’t lie. A Personal Financial Plan allows a landscape view of the future with hope for the best and preparation for the worst. Sunny days are ahead, but another storm is brewing. Any person in any relationship where income, expenses and assets are shared should pay attention to the immediate financial situation of that partnership. When change comes, knowledge is power.

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the opinions of Spire Wealth Management, LLC, Spire Securities LLC or its affiliates. Investing involves risk, including the loss of principal. Past performance may not be indicative of future results.

Spire Wealth Management is a Federally Registered Investment Advisory Firm. Securities offered through an affiliated company, Spire Securities, LLC a Registered Broker/Dealer and member FINRA/SIPC

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any strategy or investment product, or as investing advice of any kind.

Sorry, the comment form is closed at this time.